Your willpower is a finite resource; stop wasting it. True trading success comes not from fighting emotion, but from building a quantitative system that makes it irrelevant.

- Discretionary trading fails because it exposes you to predictable cognitive biases. Systematic trading builds immunity to them.

- Discipline is not an emotion; it is an engineered process of defining, testing, and automating strict entry, exit, and risk rules.

Recommendation: Stop trying to be a more disciplined trader and start architecting a more disciplined trading system.

You have been told to « control your emotions. » You have been advised to « stick to your plan. » Yet, you close winners too early and let losers run, sabotaging your own results. This is not a failure of character; it is a predictable failure of the human operating system under pressure. The common advice to simply exert more willpower is the path to ruin. It assumes your discipline is an infinite resource, which is a fallacy. The market does not reward those who try harder; it rewards those who are systematic.

The core issue is that discretionary trading places your emotional, biased brain in direct conflict with a cold, probabilistic environment. This is a battle you are statistically guaranteed to lose over time. We will not be discussing how to « feel better » about your trading. We will be discussing how to remove feeling from the equation entirely. The objective is to shift your role from a gambler reacting to blinking lights to the architect of a robust, quantitative machine.

This guide provides the blueprint for that machine. It is a strict, rules-based approach that replaces emotional guesswork with mechanical execution. We will dissect why your current methods fail, then construct, test, and refine a system that is immune to the cognitive sabotage that plagues most traders. This is not another list of tips. This is a paradigm shift. Your job is not to predict the market; your job is to follow your system’s rules without deviation.

This article provides a structured framework for building that discipline into your trading process. Each section addresses a critical component, from initial rule-setting to advanced strategy validation, guiding you from emotional chaos to quantitative control.

Summary: Applying Quantitative Discipline to Prevent Emotional Trading Mistakes

- Why Do Discretionary Traders Underperform Systematic Models Over Time?

- How to Code a Simple Trading Rule Set to Automate Your Entry and Exit?

- Backtest Results or Live Forward Testing: Which Predicts Future Success?

- The Optimisation Mistake That Creates a Strategy That Only Works in the Past

- How to Reduce Slippage by Automating Your Order Execution?

- When to Rotate from Growth to Value Factors: 3 Market Signals to Watch

- When to Rebalance: Calendar-Based or Variance-Threshold Triggers?

- Smart Beta Strategies vs Traditional Trackers: Which Fits Your ISA?

Why Do Discretionary Traders Underperform Systematic Models Over Time?

The fundamental flaw of discretionary trading is its vulnerability to cognitive sabotage. Your brain is hardwired with biases that are disastrous in a financial context. The most prominent is the « disposition effect »: the tendency to sell assets that have increased in value while holding onto assets that have declined. You lock in small gains out of fear and hold losers in the irrational hope of a rebound. This is not a personal weakness; it is a documented, predictable human behavior.

Systematic models, by their very nature, build systemic immunity to these biases. A rule is a rule. It does not feel fear when a position is up 20%, nor does it feel hope when a position is down 50%. It executes based on pre-defined, tested parameters. The data is clear: research into cognitive interventions in trading confirms that a systematic approach can lead to an 85% reduction in the disposition effect. The system acts as a circuit breaker for your worst impulses.

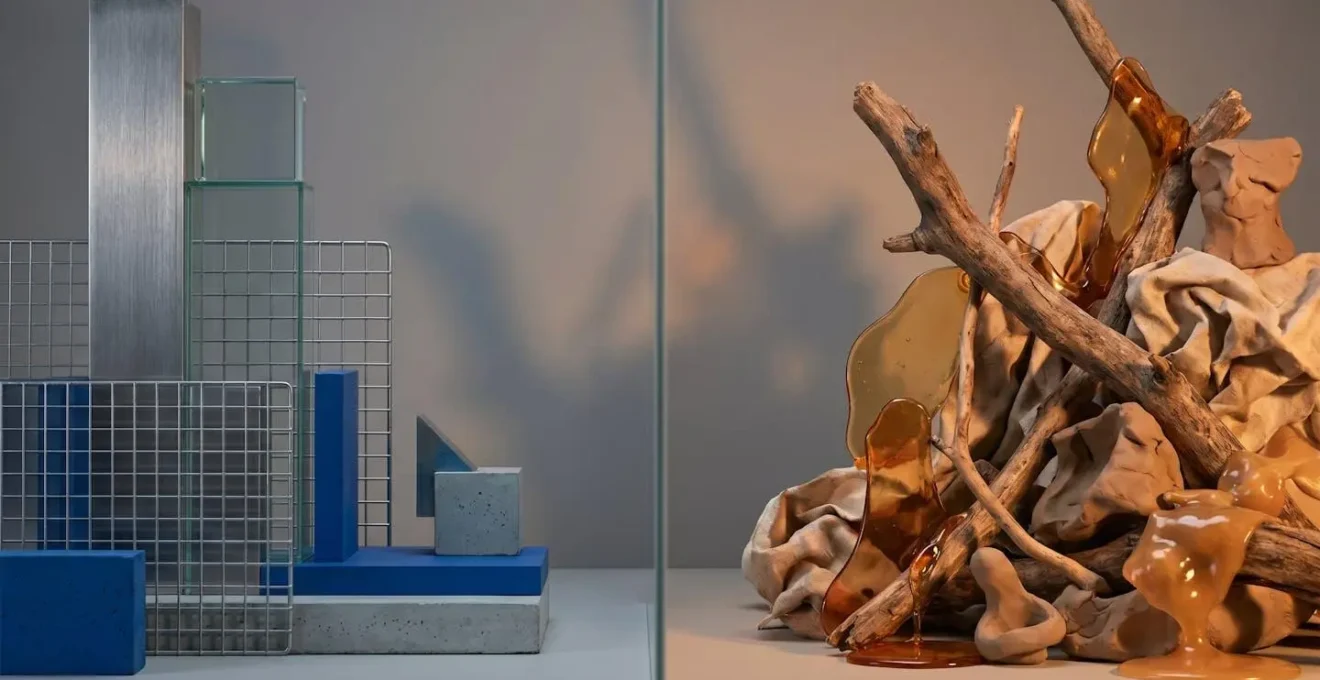

This image metaphorically represents the conflict: the chaotic, emotional impulses versus the solid, logical structure of a rules-based system. Over time, the emotional approach dissolves under pressure, while the disciplined structure remains intact. The question is not whether you are a good trader, but whether your process is robust enough to protect you from yourself. A discretionary approach leaves that to chance. A systematic approach makes discipline the default state.

How to Code a Simple Trading Rule Set to Automate Your Entry and Exit?

The transition from discretionary to systematic trading begins with externalizing your logic. You must move your trading rules from your head into a concrete, testable format. The goal is to create a set of instructions so explicit that a machine—or another person—could execute them without any ambiguity. This process of architecting discipline is non-negotiable. If you cannot define it, you cannot test it, and you certainly cannot trust it.

Start with simple IF-THEN statements for every aspect of a trade. For example: « IF the 20-period moving average crosses above the 50-period moving average AND the RSI(14) is above 50, THEN enter a long position. » This must be applied to your entries, exits, stop-loss placement, and position sizing. There can be no room for interpretation at the moment of execution. This codification of rules is the first step toward automation, which is the ultimate shield against emotional interference. As you refine your rules, you will find that data analysis reveals significantly higher win rates when trades strictly adhere to such pre-defined plans.

You do not need to be a programmer to begin this process. Modern trading platforms and third-party tools offer a pathway from low-code to full automation. The key is to first build the logic. Only then can you leverage technology to enforce it. Below is a practical plan to move from abstract ideas to mechanical execution.

Your Action Plan: From Logic to Automated Execution

- Mandatory Checklists: Before any trade, use a physical or digital checklist with Yes/No checkboxes for every rule (e.g., « Waited for candle close? », « Position size calculated correctly? »). This forces manual compliance.

- IF-THEN Documentation: Write your complete strategy logic using strict IF-THEN statements in a simple text document. This will expose gaps and contradictions in your thinking before you risk capital.

- Complex Alerts: Use the alert systems in platforms like TradingView to create multi-condition alerts that only trigger when your exact set of rules is met. This is semi-automation.

- Automation Integration: Connect your alerts to execution tools like 3Commas, Alertatron, or custom webhooks. These services translate your platform’s alerts into API orders sent directly to your broker. This is full mechanical execution.

- Regime Filters: Implement a master switch. For example: « IF the S&P 500 is trading above its 200-day moving average, THEN activate all long-only strategies. » This prevents you from fighting the dominant market trend.

Backtest Results or Live Forward Testing: Which Predicts Future Success?

A backtest is a history lesson, not a prophecy. While necessary, a simple backtest that shows stellar performance is often a sign of overfitting, not a robust strategy. It tells you what *would have* worked in a specific past that will never repeat itself. Relying solely on it is one of the most common and fatal errors in system development. The past does not perfectly predict the future; therefore, a strategy must prove its resilience on unseen data.

This is where forward-testing, or paper trading on live data, becomes critical. It is the first filter to see if a backtested strategy survives contact with the real world, accounting for factors a backtest ignores, like slippage and realistic fills. However, the superior methodology for validating a strategy’s longevity is a process known as Walk-Forward Optimization. It is the gold standard for simulating the reality of trading.

Instead of a single, static backtest over a long period, walk-forward analysis breaks the data into chunks. The system is optimized on one block of historical data (e.g., 2 years) and then tested « out-of-sample » on the next, unseen block (e.g., 6 months). This process is repeated, « walking » through the entire dataset. It simulates how a real trader must adapt, preventing extreme curve-fitting and providing a much more realistic expectation of future performance.

Case Study: The Superiority of Walk-Forward Optimization

Quantitative analysis platforms demonstrate the value of this method daily. As detailed in guides on advanced strategy validation, walk-forward optimization directly addresses the fatal flaw of static backtests. A strategy optimized over the entire 2010-2020 period might look perfect but would likely fail in 2021 because it was « curve-fit » to a specific regime. A walk-forward approach would have continuously re-optimized on rolling data blocks, adapting to changing market conditions and providing a much more honest—and typically more modest—performance expectation. This method proves a strategy’s adaptability, not just its historical luck.

The Optimisation Mistake That Creates a Strategy That Only Works in the Past

The single greatest danger in system design is over-optimization, also known as curve-fitting. This is the process of tweaking parameters until a strategy perfectly matches historical data. You add another filter, change a moving average from 14 to 12, or adjust a stop-loss by a few pips, and suddenly, the backtested equity curve is flawless. You have not discovered a holy grail; you have created a fragile, bespoke system that is exquisitely tailored to a past that will never exist again.

This strategy will fail in live trading. Its complexity becomes its weakness. Each added parameter reduces the sample size for each decision, making the results statistically insignificant. As soon as market conditions shift even slightly, the house of cards collapses. This is a primary reason why so many algorithmic strategies fail, a factor noted in market analysis which identifies that algorithm inconsistency and lack of accuracy are significant impediments to growth in the sector.

This is what an over-optimized system looks like: an impossibly complex web of rules. It is beautiful in its intricacy but utterly brittle. A simple, robust system with fewer parameters will almost always outperform a complex, curve-fit one over the long term. A key signal of this error, as noted by system design experts, is a clear warning sign. As the StrategyQuant documentation states:

If strategy performance is worse during reoptimization than the original non-optimized strategy, it is a big signal to watch for curve fitting.

– StrategyQuant Documentation, Walk-Forward Optimization Guide

How to Reduce Slippage by Automating Your Order Execution?

Slippage is the silent killer of profitability. It is the difference between the price you expected and the price at which your trade was actually executed. For discretionary traders, this is compounded by hesitation. That split-second delay while you double-check, feel a pang of fear, and finally click the button is where slippage thrives. In fast-moving markets, this hesitation can be the difference between a profitable trade and a loss.

Automated order execution is the definitive solution. A machine does not hesitate. When the system’s rules are met, the order is sent to the exchange instantly via an API. This is mechanical execution in its purest form. It not only minimizes the delay caused by human emotion and physical reaction time but also allows access to more sophisticated order types that are impractical for manual traders. These algorithms can break large orders into smaller pieces to minimize market impact or hunt for liquidity across multiple venues.

The world of institutional trading is built on this principle, constantly innovating to shave milliseconds off execution and reduce costs. While you may not have access to a Goldman Sachs trading desk, the principles and technology are becoming more accessible. The goal is to remove yourself from the execution process entirely. Your job is to design and monitor the system; the machine’s job is to execute flawlessly and without delay.

Case Study: The IS Zero Algorithm for Impact Reduction

In the constant search for better execution, firms like BestEx Research develop sophisticated tools. According to a January 2024 announcement covered in market analysis, their IS Zero algorithm was designed specifically for low-urgency trades. Instead of just following a standard Volume-Weighted Average Price (VWAP) schedule, this algorithm focuses purely on minimizing market impact. It adaptively adjusts its trading pace based on real-time liquidity, a task impossible for a human. This demonstrates the core principle: automated systems can execute strategies with a level of precision and patience that a manual trader can never hope to match, directly reducing the cost of slippage.

When to Rotate from Growth to Value Factors: 3 Market Signals to Watch

Factor investing is inherently systematic, but deciding when to rotate between factors like growth and value often falls back into discretionary guesswork. To maintain discipline, this decision must also be rules-based. You need objective, quantifiable signals that trigger a portfolio rotation, not a « feeling » that the market has topped. The three most robust signals are tied to interest rates, relative momentum, and inflation.

First, interest rate regimes are a primary driver. Rising long-term yields generally hurt growth stocks (whose valuations are based on distant future earnings) more than value stocks (which are priced on current cash flows). Therefore, a sustained, significant rise in the 10-year Treasury yield is a strong quantitative signal to begin rotating toward value. Second, relative factor momentum provides a clear market-based signal. By tracking the ratio of a value ETF to a growth ETF against its own moving average, you can identify when the underlying trend is shifting in favor of value. This removes your opinion from the equation and defers to the market’s collective judgment.

Finally, inflationary pressures directly impact factor performance. High inflation erodes the value of future earnings, making value stocks with their present-day cash flows more attractive. A rules-based approach could dynamically link the allocation to value as a direct function of the reported CPI. For example, for every percentage point that year-over-year CPI is above 2%, the allocation to value increases by 5%. These are not predictions; they are pre-defined responses to specific economic data. This is the essence of systematic trading applied to portfolio management.

When to Rebalance: Calendar-Based or Variance-Threshold Triggers?

Rebalancing is the act of restoring a portfolio to its original target asset allocation. It is a fundamental rule of risk management. The question is not *if* you should rebalance, but *when*. The two primary systematic approaches are calendar-based (e.g., quarterly, annually) and variance-threshold-based (e.g., when any asset deviates by more than 5% from its target).

Calendar-based rebalancing is simple and enforces discipline by preventing constant tinkering. It is a set-it-and-forget-it approach that guarantees you will periodically sell high and buy low. Its main drawback is its unresponsiveness. A market could crash the day after your annual rebalance, and you would be out of alignment for the next 364 days. Variance-threshold rebalancing solves this by being event-driven. It responds immediately when the portfolio drifts significantly, offering tighter risk control. However, this can lead to more frequent trading, higher transaction costs, and potential whipsaws in volatile markets.

For most systematic traders, a hybrid model is the optimal solution. It combines the discipline of a calendar with the responsiveness of a threshold. For example, the rule could be: « Review the portfolio on the first day of each quarter. Only execute rebalancing trades if any asset class has drifted more than 20% from its target allocation. » This captures the benefits of both while mitigating their weaknesses. The following table breaks down the core differences.

As this comparative analysis from market research shows, the choice of trigger has direct implications for costs and risk management.

| Characteristic | Calendar-Based Rebalancing | Variance-Threshold Rebalancing | Hybrid Model |

|---|---|---|---|

| Trigger Mechanism | Fixed dates (quarterly, annual) | Asset deviation exceeds threshold (5-20%) | Calendar review + threshold execution |

| Risk Management | Delayed response to market moves | Immediate response to drift | Balanced approach |

| Transaction Costs | Predictable, lower frequency | Variable, potentially higher | Moderate, optimized |

| Psychological Benefit | Prevents over-tinkering | Maintains discipline through rules | Combines both benefits |

| Best For | Traders prone to intervention | Risk-focused systematic traders | Most practical solution |

Key Takeaways

- Discipline is not an internal feeling but an external, engineered system of strict, non-negotiable rules.

- All trading logic must be codified into explicit IF-THEN statements before it can be trusted or automated.

- A strategy’s worth is determined by its performance on unseen data (forward-testing), not by a perfectly curve-fit backtest.

Smart Beta Strategies vs Traditional Trackers: Which Fits Your ISA?

The debate between active and passive investing often misses a crucial point. As trading coach Toby Carrodus highlights, even passive investing is a form of systematic trading.

Retail and institutional investors both underperform relative to simple benchmarks because simple investing benchmarks such as the S&P500 index are themselves rule-based systems.

– Toby Carrodus, The Psychological Underpinnings of Why Systematic Trading is Superior to Discretionary Trading

A traditional tracker, like one following the S&P 500, operates on a simple, transparent rule: buy and hold the 500 largest US companies, weighted by market capitalization. It is the epitome of a rule-based system, and its historical outperformance against the average active manager is the ultimate proof of concept for systematic investing. For a UK investor’s ISA, a low-cost traditional tracker is the baseline—a pure, disciplined, market-cap-weighted system.

Smart Beta strategies are an evolution of this concept. They are also systematic and rules-based, but they modify the weighting rules of traditional indexes. Instead of weighting by market cap, a Smart Beta ETF might weight its holdings based on factors like value (low Price-to-Book ratio), momentum (strong recent performance), quality (high Return on Equity), or low volatility. They are an attempt to build a better system—to capture market beta more efficiently or to target specific factor-risk premiums that have historically provided excess returns.

The choice for your ISA is not about « active » vs « passive ». It is about choosing the complexity of your rule-set. A traditional tracker is a simple, robust, and proven system. A Smart Beta strategy is a more complex system that makes an active bet on a specific factor. It is still systematic, but it requires you to have a conviction about which factor will outperform. For most, the discipline starts with a traditional tracker. Only once that foundation is in place should one consider layering on the complexity of factor-based rules.

The entire framework presented here is designed to achieve one objective: to build a fortress of logic and rules around your capital, protecting it from your own worst enemy—your emotional, undisciplined self. The next logical step is to audit your current trading process against this quantitative framework and identify the weakest link. Start today.